SBF: the Sovereign Individual

How the fraudulent executive was miscast as a shill for the regulatory state when reality points to the opposite

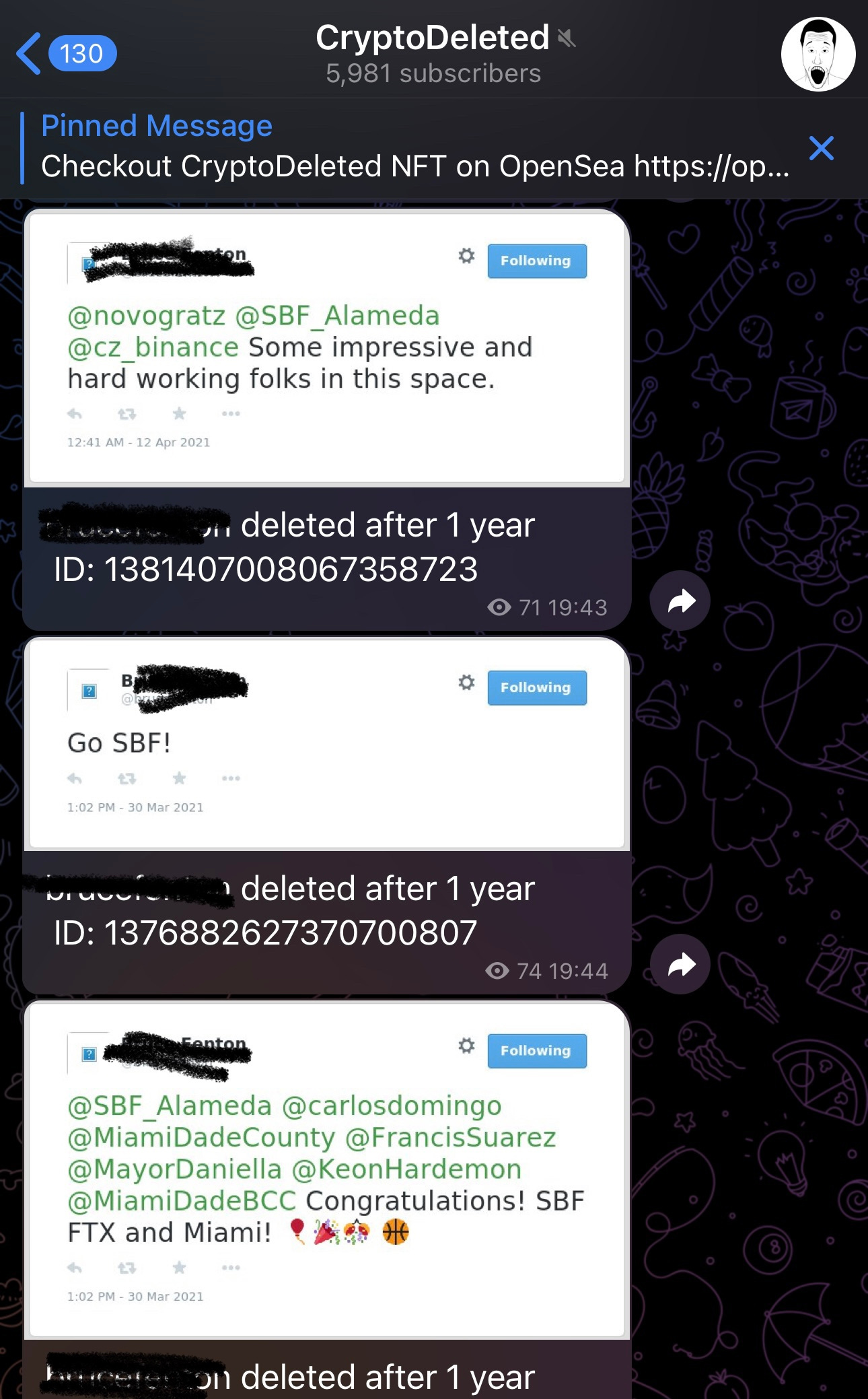

The very moment FTX collapsed in plain view, there was a mad frenzy among anyone who had ever uttered the acronym “SBF” to distance themselves from this cryptocurrency exchange and its likely criminal CEO, Sam Bankman-Fried. Thousands of tweets were deleted that previously lauded the founder, as carefully documented by the CryptoDeleted bot on Telegram. Sequoia—the most prestigious VC firm—had a 13-thousand-word profile praising SBF, which they quickly replaced. The URL for this glowing profile on the Sequoia website now points instead to a letter plainly stating that the firm regards their investment in FTX to be worthless.

SBF was also well regarded by the media and entertainment world. He maintained high profile paid relationships with professional athletes and sports teams, SBF and his co-CEO made tens of millions in donations to Democrats and Republicans, SBF championed consensus causes like climate change and sustainability, and SBF spent hours on podcasts convincingly defining his worldview as an Effective Altruist. SBF and FTX are now under investigation by the US Department of Justice, the SEC, and the House Committee on Financial Services. Reportedly, Bahamian authorities (FTX is based in the Bahamas) are discussing with US officials on possible extradition. SBF’s world is quickly unraveling, though he seems to be the last to realize this. SBF resigned and was replaced by the executive who led Enron’s restructuring. Confirming his disconnect with reality, SBF tweeted today that he is focused on “doing everything I can for FTX’s customers,” prompting the Official FTX Twitter to pushback, noting that “[SBF] has no ongoing role at FTX, FTX US, or Alameda Rsearch Ltd. And does not speak on their behalf.”

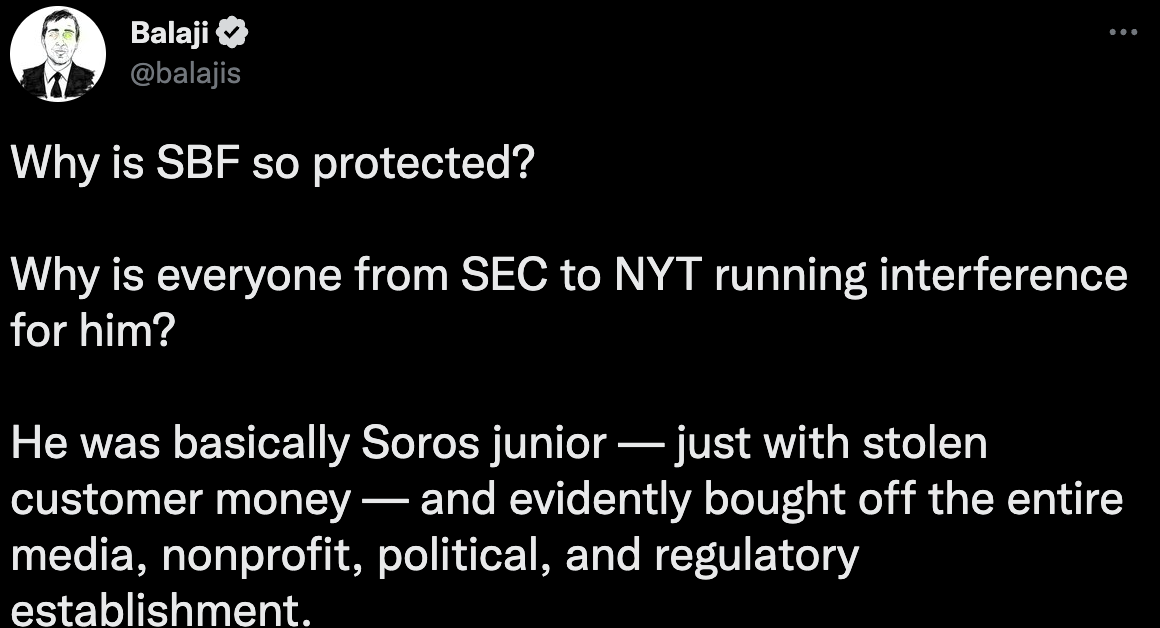

The most fascinating part of this collapse has been witnessing the rapidity and creativity with which very-online political adherents have adapted their narratives to cast SBF as the foe of their preferred ideology. The cryptocurrency community has an outspoken libertarian constituency, and almost immediately the narrative emerged that SBF was a devout woke democrat and proponent of the regulatory state. Purveyors of this worldview pointed to SBF’s millions in donations to Democrats, his stated desire to work with regulators in the United States, his professed alignment with Effective Altruism, and his association with various “liberal” causes like pandemic preparedness and sustainability. Moreover, commentators like Balaji Srinivasan asserted that the “legacy media [is] protecting SBF” because “he bought them, with what may have been customer funds.” Specifically, Balaji identified Vox, the New York Times, and others as running interference for SBF. But it wasn’t just a few publications and politicians that were protecting SBF, Balaji asserted that SBF “evidently bought off the entire media, nonprofit, political, and regulatory establishment.”

Quite a claim!

Now, many on the crypto-libertarian right go even further than Balaji Srinivasan, claiming that FTX was a money laundering operation between the Democratic Party and Ukraine to fund their war effort (an idea promoted by the former President Trump), or the sadly predicable anti-Semitic conspiracies (one of which led to the dismissal of a CoinDesk contributor). A Ukrainian official even had to take time to dispel this claim. But rather than focusing on these truly fanciful or hateful theories, I think it is better to evaluate the more conventional libertarian consensus that SBF is a big government liberal cheering on regulation, and that the harm caused by FTX are somehow downstream of the regulatory environment in the United States that prevented his firm’s entry. Then, I will propose an alternative perspective that places SBF’s worldview much closer to home for the crypto-libertarians. Namely, that up until the point that SBF commits fraud, he is actually a faithful manifestation of the “Sovereign Individual.”

It's true that SBF has called for regulation of cryptocurrencies and exchanges. He has testified before Congress, had meetings with regulators, and controversially proposed licensing for DeFi protocols. Is this evidence that SBF earnestly believes in thoughtful regulations and consumer protection? We might be left wondering this if not for excellent reporting from Kelsey Piper at Vox (interestingly, a publication previously identified as paid to protect SBF by Balaji) that revealed a DM exchange between SBF and the reporter on precisely this topic. Therein, SBF says “fuck regulators,” and “they make everything worse.” Asked directly whether it was “pretty much just PR” when “you said you wanted to make regulations, just good ones,” SBF confirmed: “yeah just PR.” On the topic of consumer protection, SBF agreed that “it would be good,” “but regulators can’t do it.” And SBF’s cynicism of regulations isn’t limited to crypto: “no one is doing it in the rest of finance, either.” “Or, for that matter, other areas that are regulated.” SBF goes on to point to the FDA, ESG, OFAC, and Big Tech regulations as other areas where institutions or regulations just “make everything worse.”

Leaving aside whether there is truth to SBF’s criticism of the FDA and other regulators, the point is clear that SBF is not a “proponent of the regulatory state.” Balaji Srinivasan called SBF “a fraud – like the regulatory state.” SBF and Balaji seem to agree on the latter! In fact, the criticism of regulators, institutions, and ESG could have easily been written by contrarian rightists like Peter Theil or David Sacks.

So why was SBF vocally supportive of crypto regulation while privately believing the opposite? It’s quite simple: SBF was trying to buy influence and goodwill (“yeah just PR”) in order to enter the US market. FTX is based in the Bahamas and serves exclusively non-US customers. FTX separately offered a severely limited US product that represented just 3% of the US crypto market share. The huge majority of the revenue (and fraud) occurred in the overseas entity. It’s clear, then, that SBF was happily profitable in the laissez faire Bahamian jurisdiction. He wasn’t asking for Bahamian authorities to step up regulations. On the contrary, SBF was on a meteoric growth path around the world in places that took a light touch “libertarian” approach to crypto regulation. And despite all of his firm’s contributions to both political parties, his reputation laundering with sports teams and celebrities, and his purported “cozy relationship” with US regulators, he ultimately failed gaining access to the US market. In the end, US citizens were mostly untouched by the collapse of FTX International—an apparent success of the US regulatory regime.

The media protection that SBF purportedly benefitted from was also short lived, if it existed at all. Today, the New York Times headline on FTX labeled the “Exchange’s Corporate Control ‘a Complete Failure,’” and the CNN headline noted the “FTX crash is eerily similar to the Bernie Madoff scandal.” Hardly the coverage you’d expect when you’ve “bought off the entire media”!

So let’s evaluate SBF instead through a different lens: SBF as the Sovereign Individual. The book The Sovereign Individual is a 1990s cult classic among libertarians and Ayn Rand acolytes that has had an outsize influence on tech billionaires (like Peter Thiel, who wrote the 2020 edition’s preface) and terminally online contrarians. The book made a number of flatly wrong predictions (eg, predicting a Y2K catastrophe and denying climate change), but also seemed prescient on certain issues, like the move to a digital economy and stateless digital money. A theme consistent throughout the book is that the most talented and profitable businessmen in a digital economy will be unconstrained by regulations and taxation imposed by artificial borders of nations, and they instead will be able to shop for jurisdictions that will minimize corporate interventions and maximize the wealth potential of the entrepreneur. Digitization enables this because operating an online service can be done anywhere in the world, especially with the advent of digital currencies and video communication. Consider these two passages from The Sovereign Individual:

Capital in the Information Age is growing more mobile by the moment. The capacity to earn high income is no longer tied to residence in specific locations, as was the case when most wealth was created by manipulating natural resources. With every day that passes, it becomes easier for people using highly portable information technology to create assets that are far less subject to the leverage of violence than any form of wealth has ever been before. Arbitrary political regulations that impose costs without creating offsetting market benefits will soon be nonviable. Powerful competitive forces are tending to equalize the prices of goods, services, labor, and capital across the globe. Governments will have less latitude to impose arbitrary policies than they are accustomed to enjoy. Any government that attempts to impose more burdensome regulations on an activity than other sovereignties will simply drive that activity away.

The triumph of capitalism will lead to the emergence of a new global, or extranational, consciousness among the capitalists, many of whom will become Sovereign Individuals. … The ablest, wealthiest persons … have the most to gain by transcending nationalism as markets triumph over compulsion. Perhaps not immediately, but soon, certainly within the span of a generation, almost everyone among the information elite will elect to domicile his income-earning activities in low-tax or no-tax jurisdictions. ... Within years, let alone decades, it will be widely understood that almost anyone of talent could accumulate a much higher net worth and enjoy a better life by abandoning high-tax nation-states.Sam Bankman-Fried is the prototypical sovereign individual. If The Sovereign Individual were a cookbook, SBF would be Paula Deen (maybe adding a zest of fraud to complement the Randian selfishness). The trajectory of his company and his personal decisions suddenly make sense when evaluated through this lens, rather than the “woke democrat regulatory shill” that he was miscast as. Sam shopped around for low tax, light touch regulatory environments for his global digital business, which he then offered to customers in every jurisdiction possible. He founded Alameda Research in 2017 in California. In March 2019 SBF moved to Hong Kong and founded FTX to benefit from the more permissive financial regulations. Despite Hong Kong’s lighter financial regulations, it was still relatively restrictive on cryptocurrencies. SBF became publicly critical of the Hong Kong regulations, and moved jurisdiction again to the Bahamas in September 2021 for the expressed purpose of taking advantage of the island nation’s crypto-friendly regime.

In the Bahamas, SBF was able to extract huge amounts of wealth through fraud and misuse of customer funds, who were located in countries around the world. He enjoyed a life of decadent luxury in a $40M rooftop penthouse with ample amphetamines and lavish parties. This same wealth was funneled to try unsuccessfully to buy influence and reputation to enter the US market. His influence campaign ended in abject failure, to the relief of would-be customers in the United States. Despite real flaws, regulatory institutions in the US prevailed.

As foretold in The Sovereign Individual, SBF sought to “accumulate a much higher net worth and enjoy a better life by abandoning high-tax nation-states” and avoid “arbitrary political regulations.” Of course, the authors never advocated overt fraud, so Sam’s selfishness went a step further. Yet, he remains a libertarian that flew around the world to evade scrutiny and maximize his wealth. The narrative that frames him as a cheerleader for the regulatory state is a misdirection meant to distract from a painful reality for the techno-libertarians: he is one of them, albeit lacking scrupels.

I really enjoyed this, and you make some excellent points.

this is excellent!